HDS Highlights

- The ‘One Hitachi’ will globalise a mix of industrial and IT businesses

- HDS has strong Unified, Virtualised and Flash Storage

- It is a good server player with UCP Integrated Systems and SMP x86 servers

- Is acquiring new customers through Managed Service Solutions

- Uses its industrial heritage to match Big Data to The Internet of Things

- Needs to make more noise through marketing

We recently attended an HDS analyst day in the UK. You’ll want to learn more about its business, offerings and plans for expansion.

The One Hitachi Strategy

Hitachi is one of the last big industrial companies to retain an IT division – not so at Siemens which has sold off almost all its interests or HP, which spun out Agilent many years ago. Samsung, Toshiba and Sony all have non-IT consumer products, but no industrial business. To pull all the strands together it has a ‘One Hitachi’ strategy, which aims to harmonise its offerings around the world.

Nakanishi-San head of Hitachi is in the process of globalising the whole company’s business and reportedly wants Hitachi to be more like HDS over time. It may seem odd that it was not always the case, but HDS CEO Jack Domme now reports directly to Nakanishi-San. Sir George Buckley (ex-3M) has also joined the board of directors.

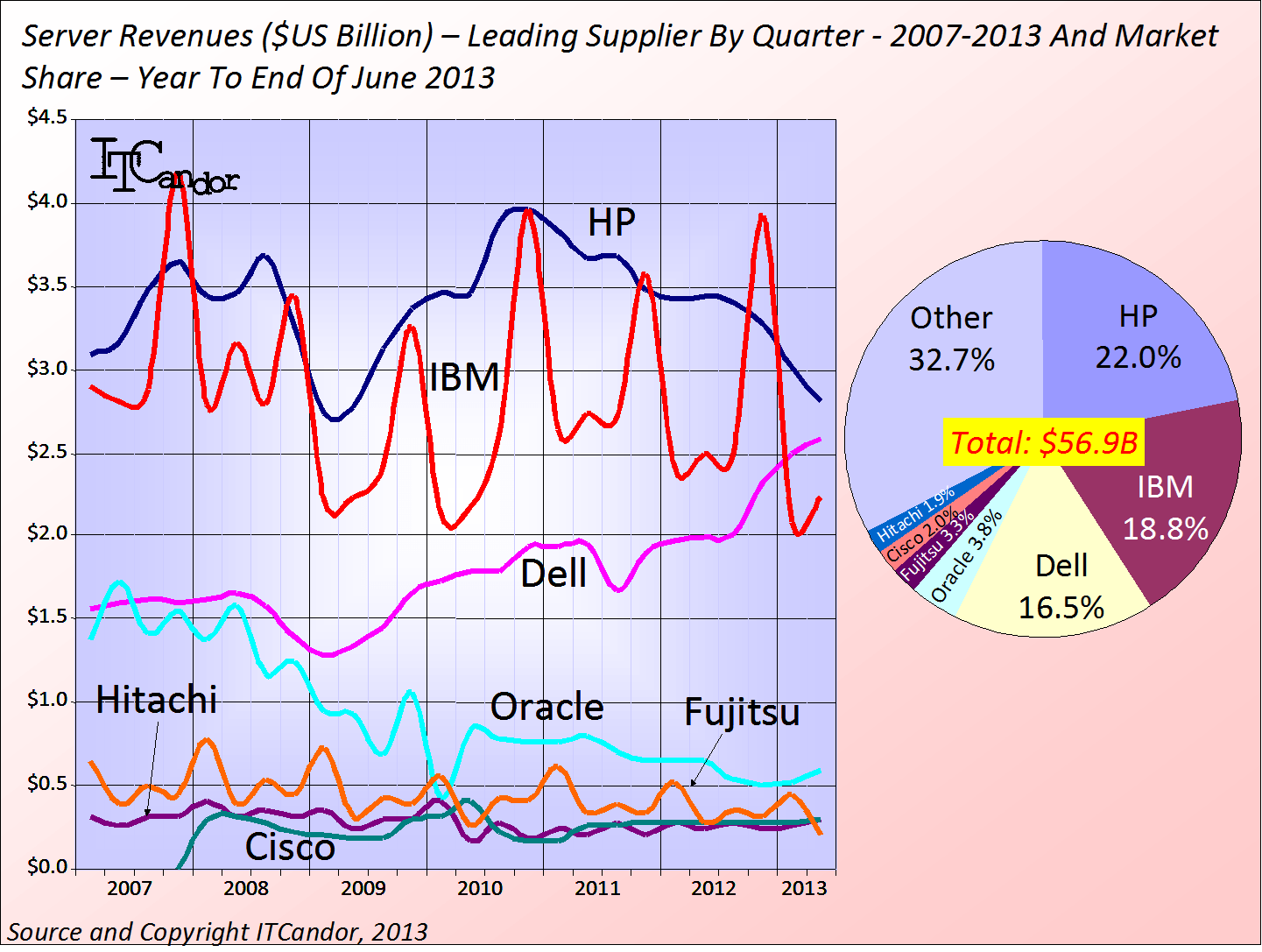

Hitachi Data Systems is one of the leaders in storage systems with a 3.7% market share in the year to the end of June (see Figure). It claims to have over 500PBs of storage under management and is building out its resources – including a new distribution centre in the Netherlands for scaling business over next 15 years. It has been a long-term supplier of automated storage and also bought NAS supplier BluArc in 2011.

The server business has been moved from Hitachi to HDS to help globalise the business. HDS has been a long-term player in servers, having at one time supplied plug-compatible mainframes under its own name and through Comparex in Europe.

HDS’s strategy focuses on 3 areas. In particular:

- Application/Information – Big Data today and tomorrow

- Data/Content – search, discover, one platform for all data

- Infrastructure – storage systems and UCP

We’ll have a closer look at its main offerings.

Storage Offerings Mix Virtualisation, Unification And Flash

HDS storage comes in 3 main types of system. In particular:

- Virtual Storage Platform (VSP) includes the Hitachi Command Suite for managing block, file and object storage. Its Controller-based virtualisation

- Hitachi Unified Storage (HUS) – HUS VM is the fastest ramping storage product in its history, with 2/3rds of sales (mainly through indirect channels) to date going to new customers. The list price of an entry level all-flash array is around $300k. Other models include HUS 110, HUS 130 and HUS 150 ranging in raw capacity from 480TB to 3.8PB. All allow the mixing of disk drives and flash, although only the VM version has expansion trays for HAF modules; during the recent analyst event HDS representatives hinted that the HUS 150 may also see this capability soon.

- Hitachi Accelerated Flash (HAF) flash devices were introduced in 2012. They incorporate MLC SSD chips – with an expected ‘durability’ of 5 years – and a built in Hitachi Flash Controller and can be incorporated in either VSP or HUS VM arrays.

In addition it offers its BluArc NAS products and has a number of file and content programmes such as Content Platform, Content Platform Anywhere, Data Discovery Suite and Data Ingestor.

HDS has a full set of offerings available and has pioneered automatic tiering and heterogeneous attachment of other vendors’ arrays. However it has been less vocal than many smaller flash vendors, who lack the depth of its approach. We believe in the past it was often more confident in talking technology than business – but that’s changing now.

Advanced Servers and Integrated Systems

In our extensive coverage of Converged Infrastructure and Integrated Systems we’ve been impressed by HDS’s approach. In particular:

- Converged Unified Compute Platform (UCP) combines compute nodes, storage and 3rd party networking from Brocade and Cisco. It claims that it takes full responsibility of the infrastructure up to the hypervisor (currently VMware, although Hyper-V is coming soon), partnering with software companies for solutions. It also resells Cisco UCS for certain applications. We position Hitachi in the middle of the vendor landscape in EMEA (See Figure). Its challenge with UCP is to gain mind-share and in positioning its offerings beyond data centre managers to CXOs. Its ‘secret sauce’ orchestration software is UCP Director, which costs between $40 and 50k.

- Compute Blade 2000 and Compute Blade 500 – despite selling around 70k blades worldwide, HDS server offerings are also not widely known. Using its mainframe experience it is the only x86 vendor to offer LPARs allowing for granular system partitioning, as well as multi-blade SMP based scaling making its servers appropriate for scale-up, applications and running large Oracle databases. The 2000 is a 10U chassis housing up to 8 Xeon E5 or E7 server blade modules, while the 500 is a 6U rack-mountable server taking up to 8 Xeon E5 blades

As with all other system suppliers HDS is actively supporting SAP HANA with certified systems as well. It claims to be the 4th or 5th largest OEM customer for SAP. Beyond HANA it supports SAP Business Suite and Warehouse on its systems as well.

HDS Services Move From Traditional To Utility Pricing

In addition to its managed storage services HDS offers a number of consulting and public Cloud offerings. In particular:

- Operational Services are the biggest part of HDS’s services business. These involve providing management of applications and data running on customer-owned equipment

- Full Managed Services include those where the customer buys or leases equipment, but wants a single SLA managed by HDS (Marks and Spencers for example)

- Managed Service Solutions as a pure consumption model, where HDS owns the equipment on the customer site and charges on a monthly utilisation on a $/month basis. HDS has managed to sign up T Systems, BMW and another 8 customers already to this new ‘customer acquisition’ model.

In addition we expect to see new Hitachi Cloud Services and/or Partner Offerings for Europe in the coming months. As with other vendors moving from Cap Ex to Op Ex offerings HDS will, of course, need to be able to handle different sales and accounting models than in the past.

Big Data From An Industrial Heritage

HDS has 200+ data scientists and offers Big Data services in Japan. It launched a Big Data Lab in April 2013 in the US with 10 data scientists. It is involved in streaming data in real-time and cell-phone network monitoring with JDSU. It is in the process of opening a Big Data Lab in Manchester, England, where it is involved in the railways (it is supplying trains to SE Trains in London) and the National Health Services, where it has a research partnership with the University of Salford. We expect to see it opening more Labs in future.

Beyond the ‘me too’ approach to Big Data analytics HDS is eyeing up the growth in machine-to-machine data, where it is in perfect position to work on the integration of digital information in industrial processes.

Some Conclusions – Growth And Modernisation

As always HDS has a lot more going on than many customers, prospects (and even many analysts) know about. It is expanding beyond storage to CIandIS and in storage – beyond spinning disk to flash, unification and virtualisation. Its business isn’t as large as EMC, IBM, HP or Cisco and it makes less noise than many flash-only storage vendors.

Its acquisition of new customers with HUS and Managed Service Solutions is very positive and it has valuable offerings based on deep experience and solid research. To progress it will need to get its messages across to a wider set of users. In its own small way we hope that this post will help.

Hi!

I am very impressed with the quality of past Hitachi products.

I particularly likedearly Hitachi CPUs (used by SUN) and hard drives (nearly as good as Seagate drives)..

To do well in the future companies must plan how they fit into the Cloud economic structure.

This has been the failure at Hitachi-technological excellence but no long term vision.

This can be fixed by managers envisioning where Hitachi fits into the Cloud era.

Smart devices like phones and screens, low cost low-energy multiCPU servers, communications, software services, search services etc. at some level, for example.

If, as I expect they fit nowhere, except in Smart devices and screen TVs they will need to find economic niches that are not dwindling to zero profits.

Like everyone else they will need to manufacture in the best economic location, not just in Japan.

Who knows, just like the small mammals came to rule the earth eventually, maybe Hitachi can emerge-or not?

Rich

Thanks for your comments as always. Talking to us is a start. The company is currently less noisy than it should be, but it is addressing the Cloud market – especially in the Managed Service Solutions mentioned in the post. It’s getting beyond the automatic storage tiering message of a few years ago. Let’s see if it can make the strategy fly.

Best Wishes

Martin

Erratta Fijitsu made the Sun CPU’s not Hitachi!

I understand you have to view things scientifically and statistically.

It is clearly hard to say what is the “Cloud” market and other market categories.

I have a view of I.T. as divided broadly into Cloud clients and Cloud servers with the Comms industry in between who are monopolising their position.

The customer is moving to the best deals available, so over-charging fat cats are on the wane.

You can by a Pay As you Go phone for £50 and a tablet for £50. When the Government buys the same items it pays £100’s of pounds.

It seems there are now two I.T. worlds, the “olde worlde” where companies are plumenting in value and desperately seek ways out from complete collapse, and the new I.T. world of Android/Linux based cloud clients and Linux-based low-energy Cloud servers. Unfortunately we are stuck with the Comms monopolies in the middle.

As I say if you can’t compete or find some niche then partial collapse is inevitable for the olde worlde I.T. companies.

Looking at clients, Apple can’t compete with Android products and has hired the ex head of Burberry to move into a luxury fashion brand niche.

I don’t believe that companies like Google, Facebook and Amazon could continue in business without bringing down costs. This means moving self-built/commissioned to low-cost low-energy servers using off-grid power.

Where does Hitachi fit into this view?

I am not initimately aware of Hitachi’s current divisions and products, I guess it is like many- stuck in the past and hesitant to abandon secure ground and jump forward into the Cloud era- and is therefore similar to Dell, HP, MS and to some extent IBM.

Due to their past technical excelence, I feel sure there are many parts of Hitachi that could become huge successes, if the management took the neccessary bold steps.

No one could envy management at all the olde worlde I.T. companies. They are caught between a rock and a hard place.