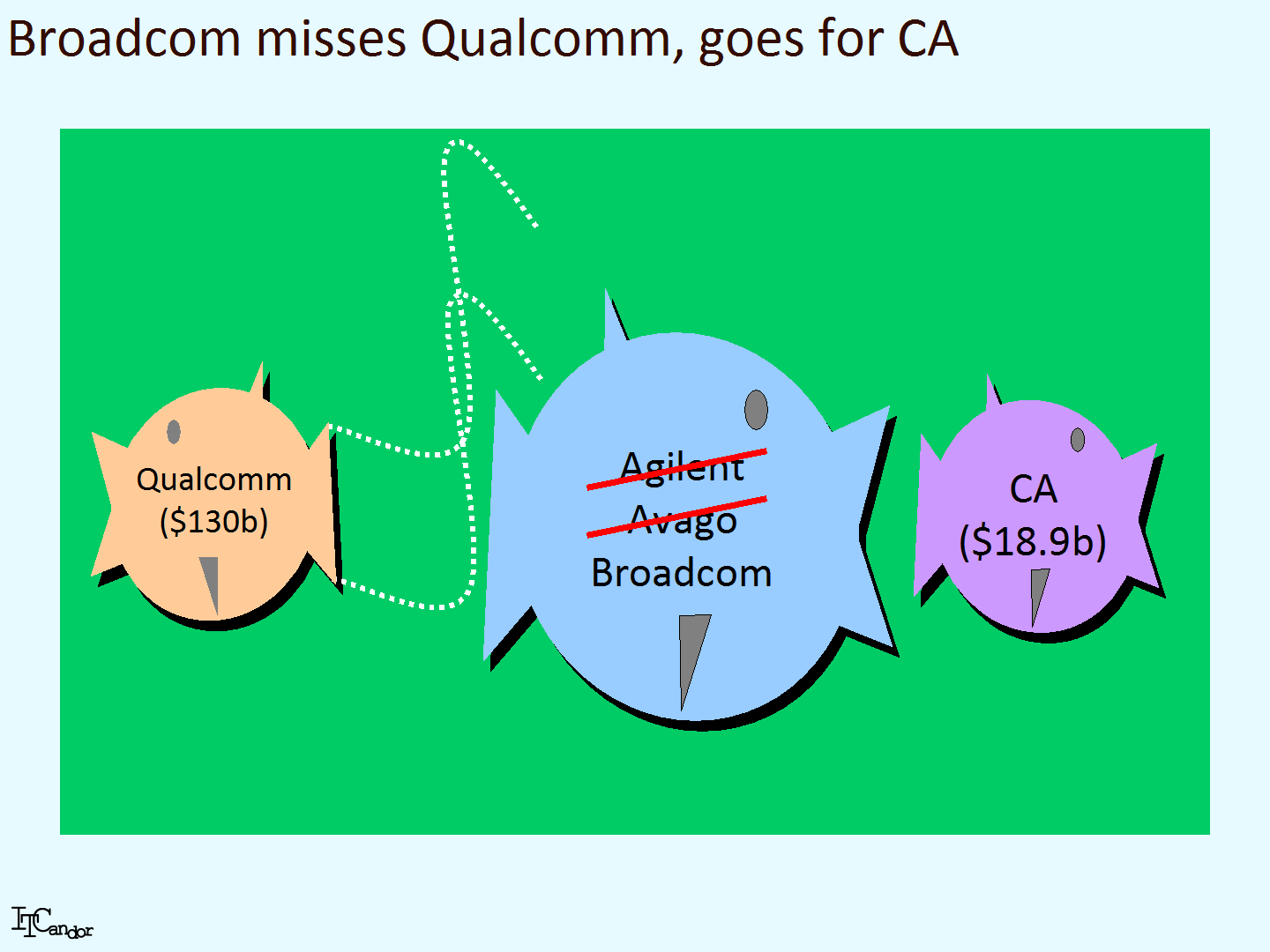

Yesterday Broadcom made a bid to acquire Computer Associates (CA) for a price of around $18.9 billion. As CA is an enterprise software and services supplier it represents a significant change in strategy for Broadcom, who hitherto (and it its various guises) has expanded its business through buying other semiconductor companies.

CA has been a major software player since its foundation in 1976; in the last year (to the end of March 2018) it made 51% of its $4.2 billion revenues from mainframe software (which in 2018 means IBM z System), 41% from enterprise solutions and 7% from services. Broadcom’s move will see it becoming a direct supplier to large end-user organisations for the first time – a major step away from its usual status as an OEM supplier of semiconductors to other vendors.

Broadcom was built through acquisitions: Silverlake Partners bought Agilent (once HP’s test and measurement division), changed its name to Avago, which then bought LSI, Emulex and Broadcom before (confusingly for some!) changing its name from Avago to Broadcom (a kind of reverse brand take-over) – see my Figure. Four month ago its ambitious attempt to buy fellow chip maker Qualcomm for $135 billion was scrapped through the direct intervention of President Trump, because Broadcom was considered to be a non-American company. His action proved my prediction that new nationalism will have increasing influence on the direction of our very global market.

In order for the acquisition to go ahead it needs to be cleared by regulators in the US, Asia and Europe. The initial reaction of the stock market has been negative for Broadcom and even if it achieves that I wouldn’t be surprised if the President vetoed the deal as he did with Qualcomm.

Broadcom’s move could bean attempt either to:

- Become a massive IT holding company with loosely connected businesses (a bit like Soft Bank which has a portfolio including ARM Holdings, Yahoo Japan and Sprint and Japanese domestic telecoms), or – more ambitiously – to

- Begin selling network and other products directly to end-users, disintermediating the market and competing against its supplier customers in the process.

It’s more likely to be the former than latter in my view. In any case it’s proving to be the most interesting IT company to watch from an financial, merger and acquisition point of view. I’m sure I’ll be writing about it again soon.

{kind=link}

One Response to “Broadcom bids for CA – enters the enterprise market”

Read below or add a comment...