The server market is large ($82b in the year to the end of June), growing (+8.9% in the year and +12.7% to $22b in Q2); unit shipments grew by 9.6% in the year to 26m and by 14.1% in the quarter to 7m; the installed base at the end of June grew 4.0% to 77m. Dell was the largest vendor (see my Figure above), non-virtualised servers still accounted for the majority of revenues (57.25), while x86 processors accounted for 85.6% and Microsoft Windows, 71.9%. However a significant proportion of servers, using approximately 10m server processors, are self-built by large cloud service providers, which has substantially reduced the market for branded products which are the subject of this research paper.

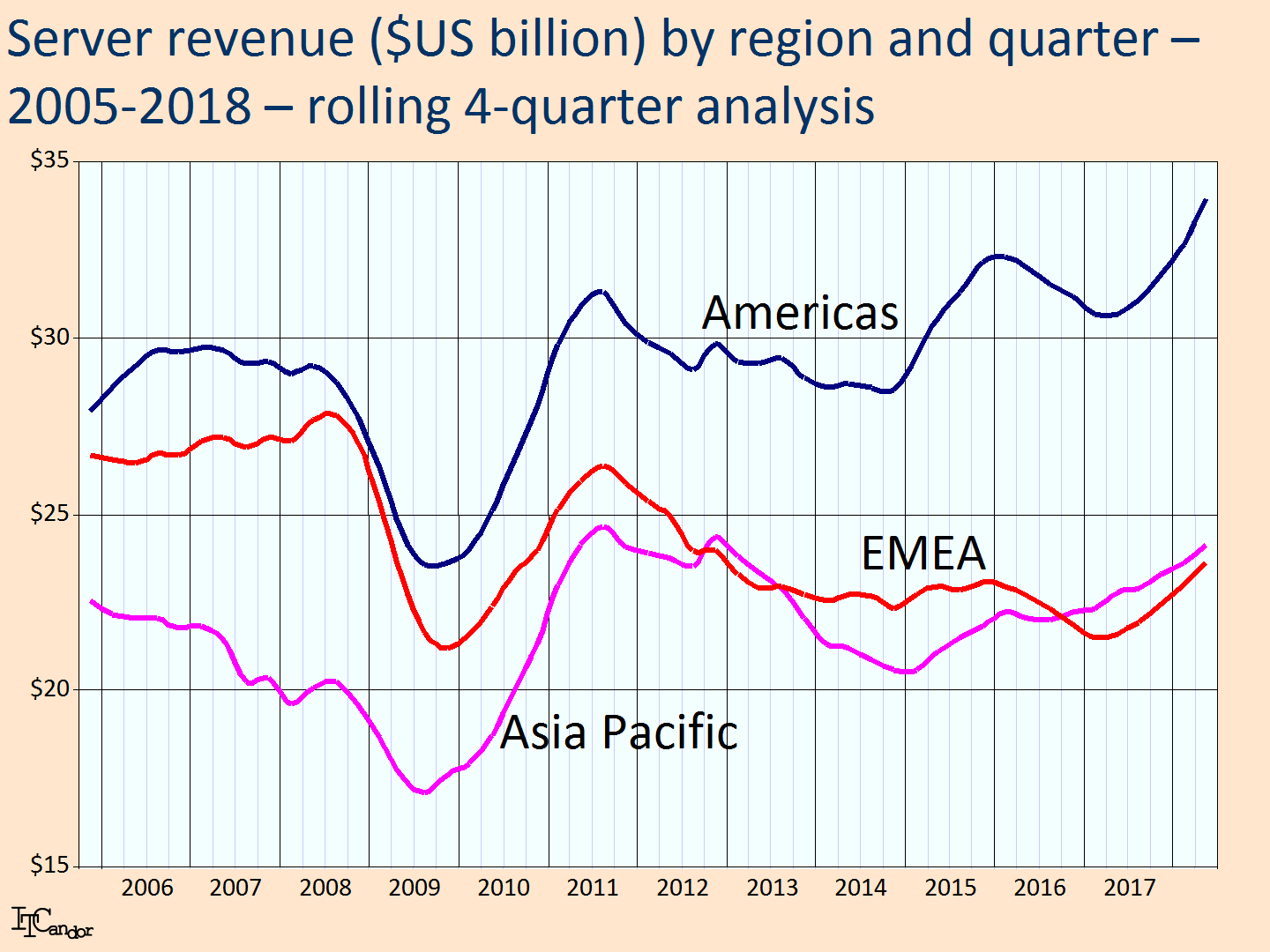

The Americas (and the USA in particular) has always been the strongest of the regional markets for servers. My Figure above shows the development of revenues/spending in current dollars since 2005 on a rolling 4-quarter basis. It is clear how badly affected the server market was by the Credit Crunch in 2008-9, the recovery in 2011-16 and the extra growth – partially due to new processors from Intel, AMD, IBM and Oracle – in 2017-18. I expect spending at a regional level to reach another plateau later this year with even stronger growth being snipped away by the self-building mentioned above.

In my Figure to the left I show regional growth on a local currency basis (using the Euro for EMEA and Chinese Yuan Renminbi for Asia Pacific), again on a rolling 4-quarter basis. Here we see again the short, sharp decline and recovery caused by the Credit Crunch and the subsequent recovery, which was much stronger in EMEA than the other two regions in 2015.

In my Figure to the left I show regional growth on a local currency basis (using the Euro for EMEA and Chinese Yuan Renminbi for Asia Pacific), again on a rolling 4-quarter basis. Here we see again the short, sharp decline and recovery caused by the Credit Crunch and the subsequent recovery, which was much stronger in EMEA than the other two regions in 2015.

Asia Pacific had stronger growth in 2016-17, while it and EMEA have shown weaker growth in 2018; the comparative strength of the – due partially to the extra spending in the USA created by the significant tax cuts at the end of 2017. I don’t believe that either EMEA or Asia Pacific will overtake the Americas as the largest region for server sales anytime soon.,

I reported last quarter that Dell had eventually overtaken HPE as the world’s largest server vendor – a lead it increased in Q2 on a rolling 4-quarter basis (see my Figure above). IBM’s rapid decline and Lenovo’s growth was caused by the latter off-loading its x86 server products of cause. Oracle has grown its server business in recent quarters, as has Huawei, which has the best chance of overtaking IBM as the third largest server supplier in the next two years.

Cisco’s server business reached a plateau in 2015; it doesn’t look likely to increase its revenues significantly unless it expands its product range beyond the rack-based UCS systems it supplies today and the relationship its has with IBM, Dell EMC and NetApp to add its network and software components to their hyper-converged infrastructure (HCI) systems.

My challenge for the slimmed down HPE, consolidated Dell and other server vendors is to make their services and products more relevant for use by cloud service providers (CSPs) whose IaaS and PaaS services are growing at 30% a year. Supermicro – the eighth largest server vendor – achieved over 30% revenue growth in the quarter and year, demonstrating that it is the only one managing to surf the current surge in cloud service adoption. While AWS, Microsoft Azure, Google and a handful of other large CSPs will non-doubt continue to make their own systems, there are hundreds of other smaller CSPs who never will.