Server Highlights

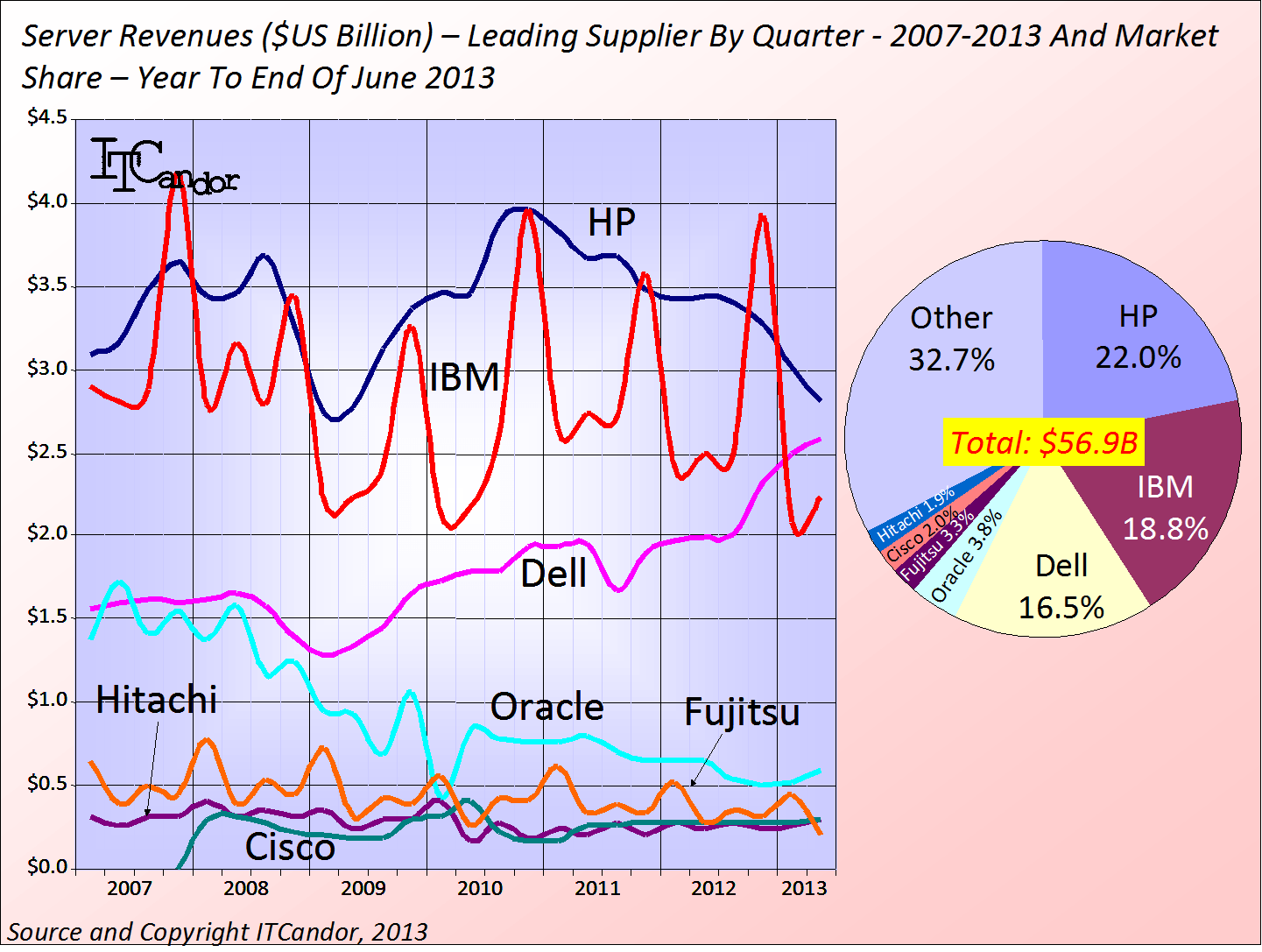

- The market fell 3% to $13.4B in the quarter and by 2% to $56.9B in the year to the end of June

- HP was the leader with a 22.0% share for the year from its $12.5B revenue

- IBM was in second with 18.8% from $10.7B

- Dell overtook IBM in the quarter, but remains behind IBM on an annual basis achieving a 16.5% share from $9.4B revenues

- There were 3.6M shipments in the quarter and 14.6M in the year

- The installed base reached 44.9M

- Virtualised servers grew 11% to $6.2B, while physical-only machines decline 13% to $7.2B

- 36% of the $10.4B spent on x86 servers was for virtualised machines

- VMware hypervisors accounted for 63.6% of x86 hypervisor revenues

It’s time to take a look at market developments in the server market in Q2. We’re encouraged to find that revenues declined by just 3% against the previous year – a much better result than the constant -7% decline in the previous 3 quarters. So many current strategies involve the acquisition of servers, whether integrated systems and converged infrastructure, VDI, Big Data or mobility.

Shipments grew by 3% to 3.6 Million units, underlining the extent to which customers get ‘more for less’ from servers due to the significant improvements in processor capabilities over time. The installed base also continues to grow – this quarter by 7% to reach 46.8 Million.

In terms of suppliers the long-term dual hegemony of HP and IBM is at last being threatened by the rise of Dell. HP has maintained its lead for now on both an annual and quarterly basis, holding a 22.0% share of the annual market to the end of June (see Figure). IBM, on the other hand, has maintained a strong number 2 position in annual sales (18.% from $10.7 Billion revenues), but has been overtaken by Dell in the quarter. Dell held a 16.5% share from revenues of $9.4 Billion for the year. As in other areas IBM’s revenues have a heavier Q4 skew than others and it is now seesawing against Dell in the way it used to against HP. We see no reason why Dell shouldn’t eventually overtake IBM and even HP in the server market, as this is one area where its new strategy is working well.

Virtualisation continues to grow: of the $10.4 Billion spent on x86 machines 36% were for virtualised machines verses the 66% for physical-only machines. VMware continues to rule the roost in terms of hypervisors deployed, holding a 63.6% share in the quarter. Microsoft, KVM and Xen had 12.&%, 11.4% and 11.1% of that market respectively.

Across all server types virtualisation grew by 10% to $6.2 Billion and accounting for 46% of total revenue in the quarter. Physical-only servers declined by 13% to $7.2 Billion.

It was a horrible quarter for Unix machines with revenues falling by 21% to $1.4 Billion, while System z revenues grew by 10% (see our earlier review. Windows servers declined by 1% to $9.1 Billion – a poor return given the introduction of the 2012 version last year. Linux revenues grew by 1% to $1.1 Billion.

It’s going to be an interesting ride going forward as new converged infrastructure and integrated systems are positioned by vendors to automate manual process and reduce spending on internal staffing costs as a result. There will be increased competition between suppliers as a result as they try to win a larger slice of data centre budgets. We expect integration to spread to branch office systems as well over time. We expect some serious repositioning of Sparc, AIX, i5/OS and Itanium servers as integrated systems as their vendors strive to counter their current unpopularity.

If you want to use more of our statistics in your business planning why not subscribe to our tracker?

One Response to “Server Markets Drop Just 3% In Q2 2013”

Read below or add a comment...