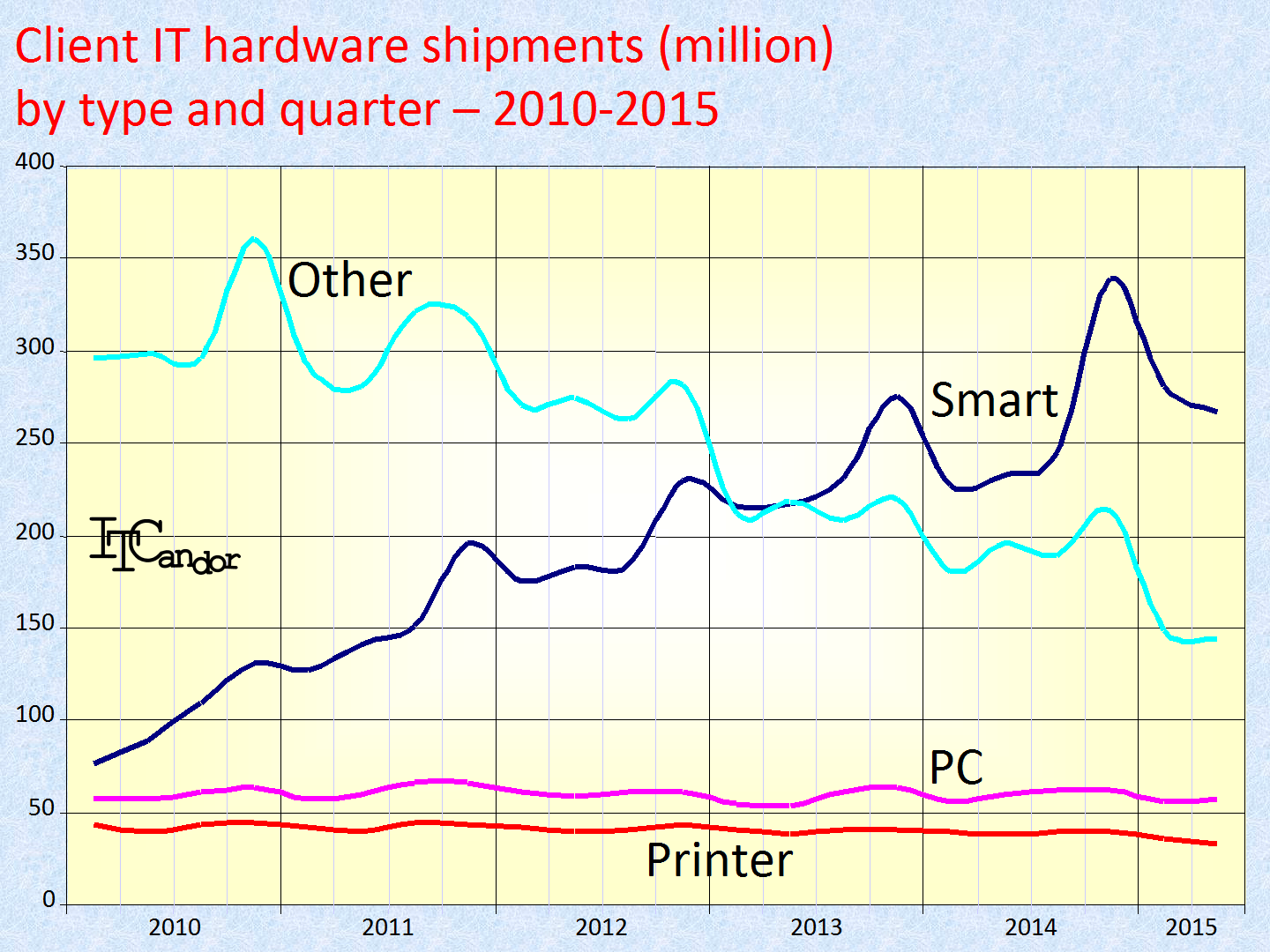

Following our analysis of market shares for client devices by type last week, I wanted to share the shipment perspectives with you. This bulletin is designed for those of you who these markets measure success and opportunities in unit terms. In total there were 2.2 billion shipments of client hard devices in the year to the end of June – up 2.1% on the previous year. Smart devices predominate (see the Figure), having overtaken ‘other’ devices in 2013. See my earlier article for definitions of what’s included there.

Over half (51.5%) of client hardware devices shipped were Smart – typically running an ARM chip and either iOS or Android operating systems. While the majority of these in turn were phones and tablets, we’re beginning to see the rise of wearables and IoT devices. From this unit perspective PCs accounted for only 10.8% of shipments. In the year there were 239m PCs shipped – the exact same number as the year before. Printers accounted for 6.7% of shipments, declining from 7.3% in the previous year.

Over half (51.5%) of client hardware devices shipped were Smart – typically running an ARM chip and either iOS or Android operating systems. While the majority of these in turn were phones and tablets, we’re beginning to see the rise of wearables and IoT devices. From this unit perspective PCs accounted for only 10.8% of shipments. In the year there were 239m PCs shipped – the exact same number as the year before. Printers accounted for 6.7% of shipments, declining from 7.3% in the previous year.

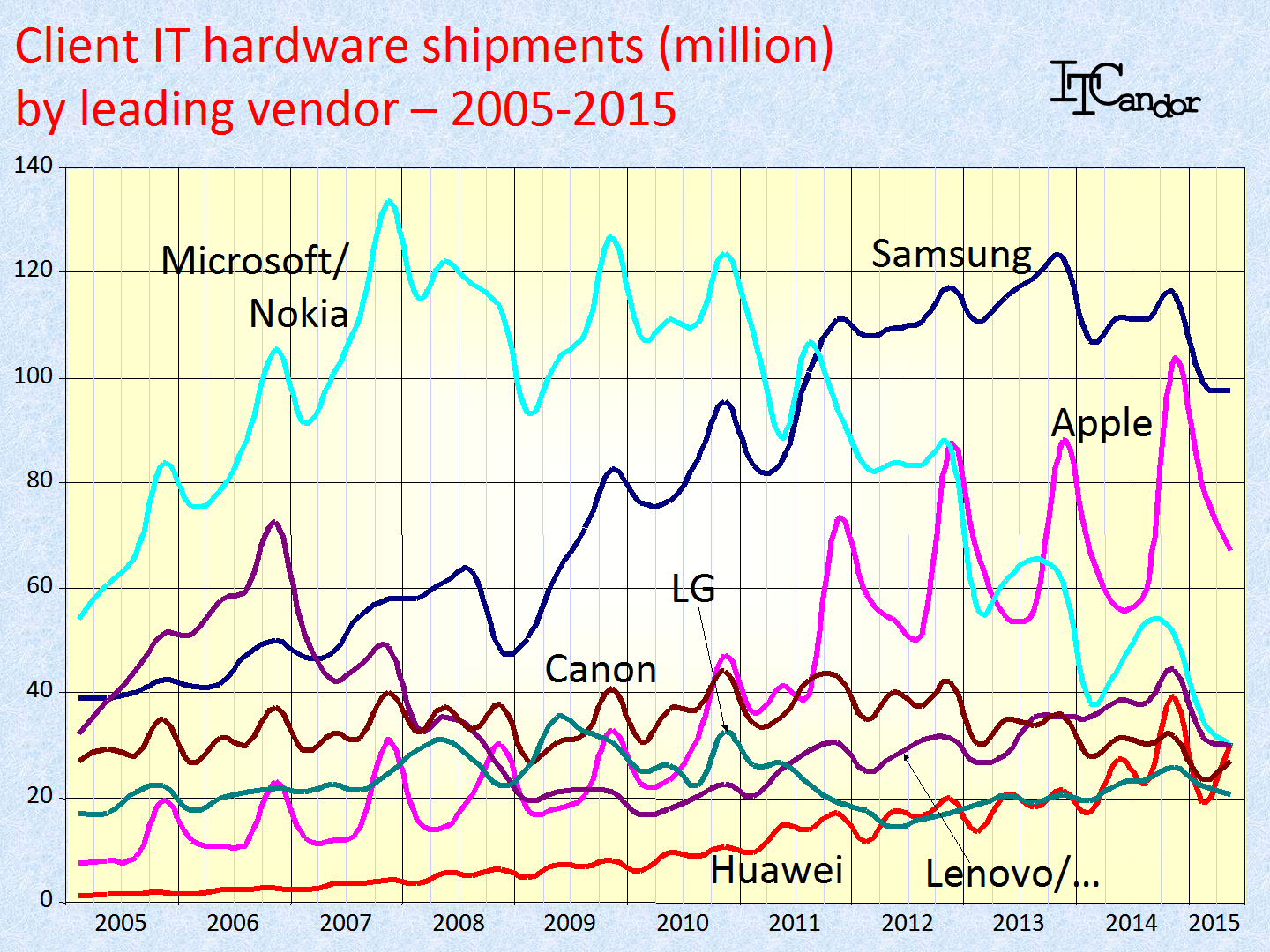

Samsung shipped most in the year – 423m devices gave it a 19.1% share. Apple has a reputation for high prices; nevertheless it still came in second – 310m shipments giving it a 14.0% share. Microsoft’s acquisition of Nokia’s mobile business took it from nowhere to become the third largest supplier of client devices with a 7.7% share; however its focus on ‘smart’ rather than ‘basic’ mobile phones will probably see its share decline in the near future. Chinese vendors Huawei (5.1%) and Xiaomi (4.2%) sell lower-priced devices and so have a stronger position in shipment (than revenue) market shares.

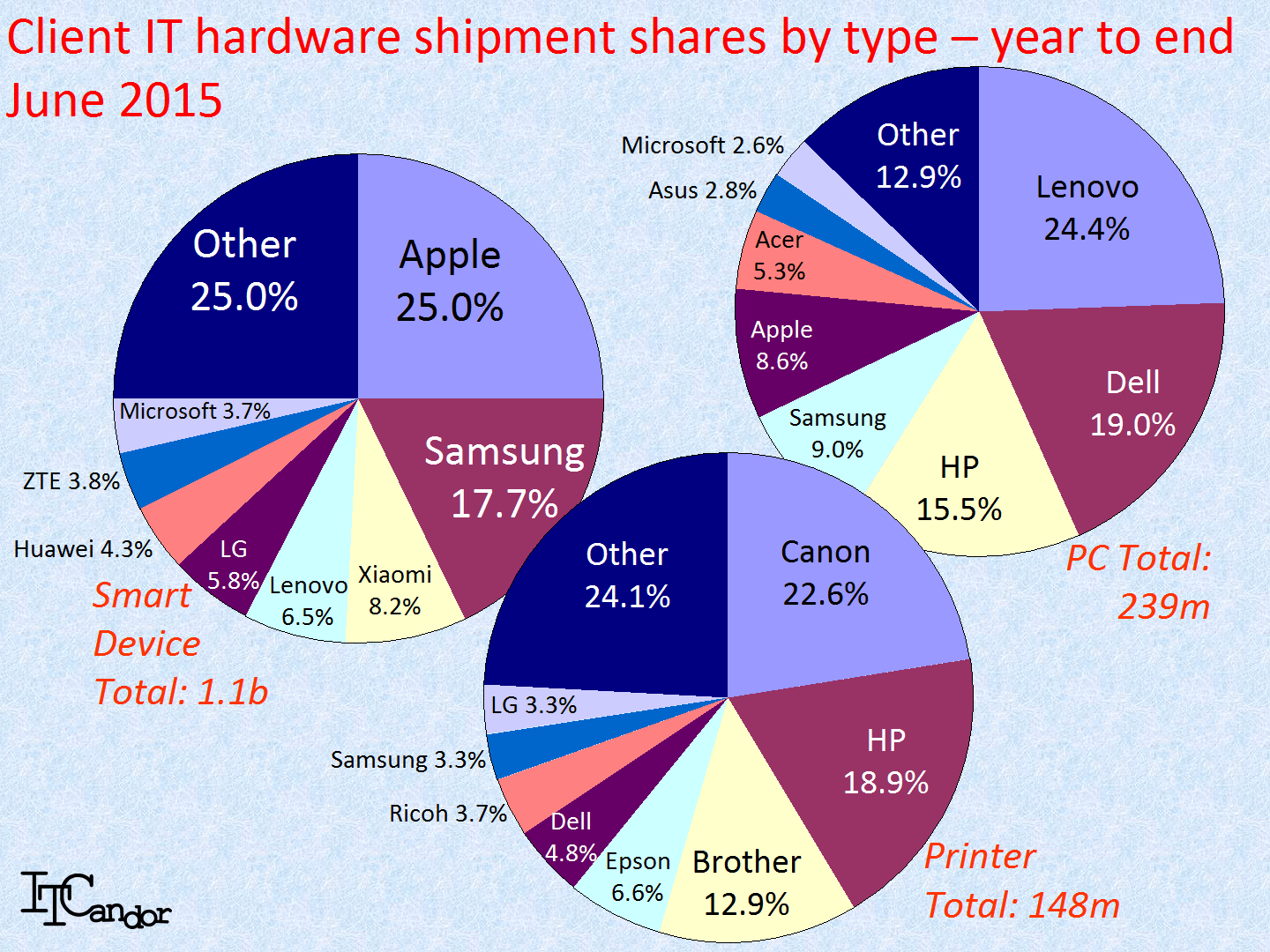

Breaking the 2.2b shipments down further, I’ve included shipment shares for smart devices, PCs and printers in the Figure opposite. The only difference in leaders is that Canon is top (rather than HP) in printer shipments for the year. Apple’s unit share (25.0%) in smart devices is exactly half of its revenue share. Chinese vendors Xioami, Lenovo, Huawei and ZTE have significant shares of shipments in smart devices, but (with the exception of Lenovo’s leadership of the PC market) are almost entirely absent elsewhere. By avoiding participation in the older, more mature, client hardware markets they have less reliance on Microsoft and Intel in the PC market and in making significant R&D investments in designing laser and ink jet printers. On the other hand they have much more dependence on Google’s Android operating system and ARM chips.

Breaking the 2.2b shipments down further, I’ve included shipment shares for smart devices, PCs and printers in the Figure opposite. The only difference in leaders is that Canon is top (rather than HP) in printer shipments for the year. Apple’s unit share (25.0%) in smart devices is exactly half of its revenue share. Chinese vendors Xioami, Lenovo, Huawei and ZTE have significant shares of shipments in smart devices, but (with the exception of Lenovo’s leadership of the PC market) are almost entirely absent elsewhere. By avoiding participation in the older, more mature, client hardware markets they have less reliance on Microsoft and Intel in the PC market and in making significant R&D investments in designing laser and ink jet printers. On the other hand they have much more dependence on Google’s Android operating system and ARM chips.

{kind=link}

Differences in technology makes it difficult for a vendor to succeed in multiple areas: Samsung has a presence in all three, but HP, Dell, Lenovo and Canon are each absent from at least one.

Looking at shipments on a quarterly basis the strongest movements have been the decline of Nokia/Microsoft, the rapid growth of Samsung and Apple and the strong fourth-quarter seasonality of Apple’s business (See Figure). Lenovo’s acquisition of Motorola’s phone business from Google hasn’t given it a substantially better shipment position, while Huawei continues to grow rapidly – albeit from a reasonably low base.

Looking at shipments on a quarterly basis the strongest movements have been the decline of Nokia/Microsoft, the rapid growth of Samsung and Apple and the strong fourth-quarter seasonality of Apple’s business (See Figure). Lenovo’s acquisition of Motorola’s phone business from Google hasn’t given it a substantially better shipment position, while Huawei continues to grow rapidly – albeit from a reasonably low base.

It’s interesting that unit shipments grew less than revenue in the client hardware market (2.1% verses 4.6%), underlying the move towards higher-priced, more-intelligent devices. PCs and printers remain more hardwired and less ‘software defined’ than smart phones, tablets and wearables. Products dedicated to a single function will grow as the market for IoT devices blossoms of course.

All of our data for client devices is available at a regional or country level – so let me know if you’re in need of something specific for you business planning. This information is updated on a quarterly basis and is available from us as a service. Please fill in your details to download the flyer and order form.

[email-download download_id=”12617″ contact_form_id=”12619″]

One Response to “Client IT hardware devices – the shipment perspective”

Read below or add a comment...