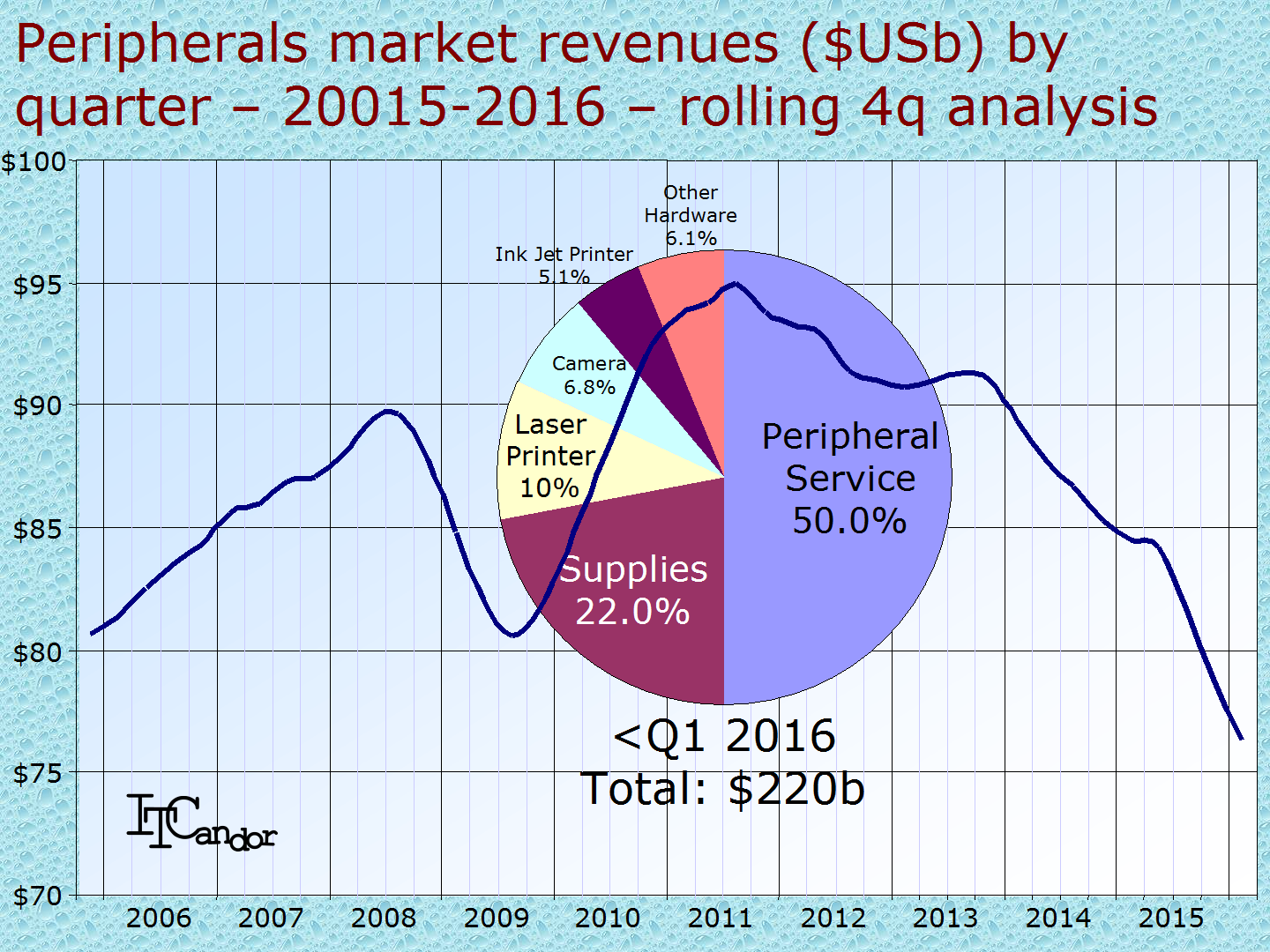

The peripherals market continues to disappoint – declining 11.7% in the year to the end of March 2016 and by 8.9% to $53b in Q1 2016. Naturally the definition of ‘peripherals’ contains many different items, which we split into 6 classes (see Figure). This is a mature market with 70% of investments made in services and supplies. Printers (ink jet and laser) were just 15.1%, digital cameras 6.8% and other hardware (including mobile speakers, keyboards and mice) were 6.1%. You’ll want to learn more about how the vendors have been performing.

Printer revenues declined by 13.4% in the quarter to $7.9b and 15.3% in the year to $33b.

Printer revenues declined by 13.4% in the quarter to $7.9b and 15.3% in the year to $33b.

There was no change in leadership in the last year in the printer market – as always Canon and HP led the other vendors, as they did in overall peripherals markets. Canon held a 20.1% share of the total $33b revenues and 22.7% of the 135m unit shipments (see Figure). HP Inc. held 19.7% and 17.8% of these respectively. Brother, Xerox, Ricoh, Kyocera and Epson held positions 5 to 7 respectively.

Reasons for declining sales include users no longer needing to print hardcopies of documents to make up for poor computer screen resolution, an increase in online and email communication from letters and postage and a lack of new technical development in the classic printer market. Sales are also suffering from the move away from PCs to tablets and smart phones: printers are typically desk or office bound and are less relevant to an increasingly mobile computer world.

None of the leading vendors grew their businesses in the last year (See Table which gives a comparison of market shares for the year to the end of March 2015 and 2016).

{kind=link}

Table – Peripherals market shares ($USb) – year to end of March 2015 and 2016

| <Q1 2015 | Share % | <Q1 2016 | Share % | Growth % | |

| Canon | $48.2 | 19.4% | $44.1 | 20.1% | -8.4% |

| HP | $44.9 | 18.0% | $39.2 | 17.9% | -12.6% |

| Ricoh | $18.6 | 7.5% | $17.0 | 7.8% | -8.6% |

| Samsung | $16.6 | 6.7% | $15.3 | 7.0% | -8.1% |

| Epson | $12.9 | 5.2% | $12.0 | 5.5% | -7.0% |

| Hitachi | $11.8 | 4.7% | $11.1 | 5.1% | -5.5% |

| Xerox | $17.4 | 7.0% | $10.6 | 4.8% | -39.2% |

| Konica Minolta | $11.0 | 4.4% | $9.8 | 4.5% | -11.2% |

| Brother | $8.3 | 3.3% | $7.6 | 3.5% | -7.9% |

| Lexmark | $6.3 | 2.6% | $5.6 | 2.6% | -11.6% |

| Dell | $5.9 | 2.4% | $5.6 | 2.5% | -5.0% |

| Kyocera | $5.3 | 2.1% | $4.7 | 2.1% | -11.1% |

| Other | $41.3 | 16.6% | $36.8 | 16.8% | -10.9% |

| Total | $248.6 | 100.0% | $219.5 | 100.0% | -11.7% |

Of course growth rates look worse in current dollar than they would in the local revenues (largely Japanese Yen) of most peripherals vendors. Xerox revenues declined more than most as it disposed of its paper supplies business in North America and Europe, sold its outsourcing business to Atos and prepared to split the company. HP Inc. was split from HP Enterprise in the autumn with the intention of increasing revenues and profits from the greater focus each new company would have: we have not yet seen the benefit in the peripherals area, which is has been a major profit contributor to the combined company for years. Xerox’s decision to downsize is an indication that even the high profitability from services is no longer considered to be enough. At least the business in dollars will start to look better for Asian vendors as exchange rate fluctuations have lessened – at least for now.

One Response to “Peripherals sales down 8.9% in Q1 2016”

Read below or add a comment...