It took many vendors by surprise when users began to prefer their mobile phones to PCs for accessing and interacting with the Internet. Over the last decade mobile devices of all sorts have outgrown all other hardware markets. You’ll want to learn more about the way this market is developing.

In 2015 the market was worth $389b in revenues for 1.6B shipments; while the installed base reached 3.7B. The Figure shows the shipments (in millions) of each type of mobile device by quarter. Most notable was the rapid rise of basic phones and the – even sharper – rise of smartphones, which became the predominant sector at the end of 2013. Classifying phones into basic and smart categories is somewhat a matter of taste (one man’s ‘smart’ is another man’s ‘basic’); however the addition of browsers, compute power and the proliferation of apps was a game changer. Nokia, Motorola and Blackberry lost out to Samsung, Huawei and – above all – Apple. In the recent past a lot of horses have been changing riders: Google bought Motorola’s business before selling it on to Lenovo, while Microsoft acquired Nokia’s mobile division: both of these movements accelerated the shift from basic to smart.

At a regional level the Americas and Asia Pacific each accounted for 39% of the world market: EMEA customers took just 24% of the business (see Figure for the quarterly shipments of all mobile devices by region from 2005). There are still relatively under-developed markets in India and Africa, but for the most part those buying mobile devices are replacing or adding to phones and tablets they already have. China is an interesting market with Apple’s recent success balancing a fall in sales from indigenous suppliers. I don’t believe that smart wearables are going to make a lot of difference: like tablets I expect they will reach their peak significantly before and below the phone market itself.

At a regional level the Americas and Asia Pacific each accounted for 39% of the world market: EMEA customers took just 24% of the business (see Figure for the quarterly shipments of all mobile devices by region from 2005). There are still relatively under-developed markets in India and Africa, but for the most part those buying mobile devices are replacing or adding to phones and tablets they already have. China is an interesting market with Apple’s recent success balancing a fall in sales from indigenous suppliers. I don’t believe that smart wearables are going to make a lot of difference: like tablets I expect they will reach their peak significantly before and below the phone market itself.

Users are gaining a richer experience than ever from their mobile devices with new offerings (such as Apple Pay) signalling a shift in revenue from hardware to services. The telecom suppliers have been lacklustre in their attempts so far to take advantage of the mobile device wave – I expect them to try harder in future.

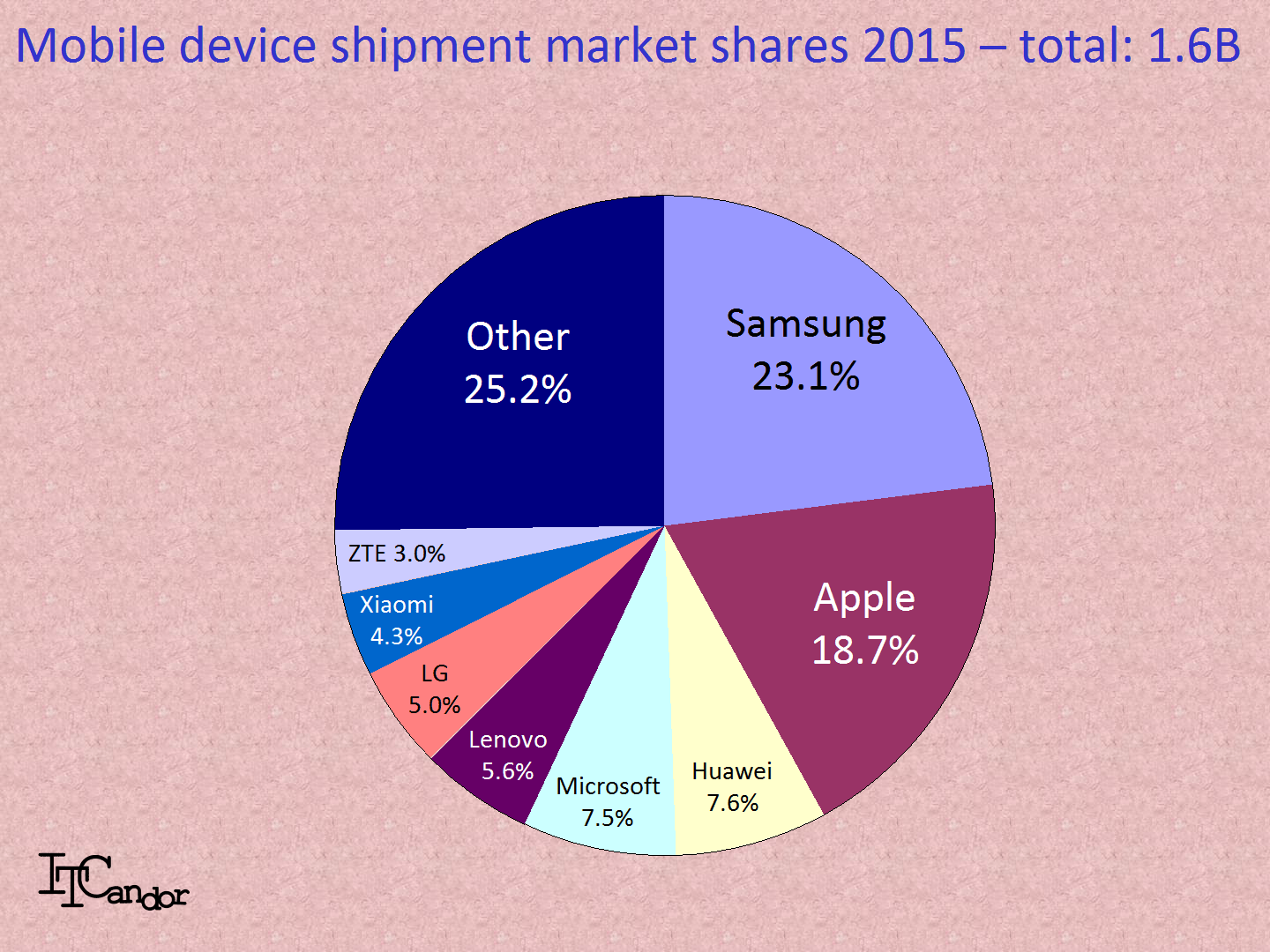

Apple only does smart and was the market leader in terms of revenues, taking 44.7% of the total business in 2015. Samsung however sold more units (see Figure), taking a 23.1% share versus Apple’s 18.7% in the year. Huawei (7.6%), Microsoft (7.5%), Lenovo (5.6%), LG (5.0%), Xiaomi (4.3%) and ZTE (3.0%) took the other major places.

Apple only does smart and was the market leader in terms of revenues, taking 44.7% of the total business in 2015. Samsung however sold more units (see Figure), taking a 23.1% share versus Apple’s 18.7% in the year. Huawei (7.6%), Microsoft (7.5%), Lenovo (5.6%), LG (5.0%), Xiaomi (4.3%) and ZTE (3.0%) took the other major places.

6 of the major vendors are Asian and 2 American. Nokia’s withdrawal took away Europe’s only vendor, which partially explains the slower sales in that region.

The future is going to be interesting, as all types of device apart from smart wearables have peaked. Business plans need to address selling more to the same customers rather than the mass expansion Eastwards of the past. I’m particularly interested in the development of business applications in maintenance, purchasing and security as well as the evolution of mobile payments. It will also be interesting to see if Gigaset will be able to establish itself as a major European player.