Cisco C-Scape Highlights

- Restructured to address generational issues in 2005

- Should deliver stronger end-of year results than either IBM or HP

- Not driving UCS towards workloads and appliances

- Has 5 ‘architectures’, but no overall mission target

- Cloud Computing strategy good for Telecom hosting in Europe

Cisco’s held its C-Scape analyst meeting this week at the Excel conference centre in London’s East End, just a mile from the stadium being built for the Olympics in 2012. Cisco is a main sponsor of the games, so its UK profile is likely to grow over the coming months.

A highlight of the event for us was CEO John Chambers’s presentation and discussion. He has a disarmingly personable style, actively engaging with 100 or so in the C-Scape analyst event and with the 2.5k developers and users in the Cisco Live! Main auditorium. He listens well, admits when he doesn’t know a specific answer and offers to follow up in areas of particular interest to him.

We thought it would be interesting to look at the company’s direction, strategy and market challenges.

What Will Cisco’s Q2FY11 Look Like?

Chambers made the necessary point that he could not in any way comment on Cisco’s latest quarterly results, but we thought it would be fun to speculate.

Cisco has managed some substantial growth in the last few quarters, growing by 8%, 27%, 27% and 19% adding to 20% growth for the year to the end of its 1st quarter. Net profit growth has been even stronger at 38% for the same period. Unlike the company itself we can speculate on its latest quarter (ending in January). We believe its revenues will be shown to have grown by 17% to $11.5 billion and its net profit by 10% to $2.0 billion. If we’re right it will mean that the company has done better than the latest published of IBM (revenues up 3% and net profits, 12%) and HP (8% and 5% respectively). Of course all three vendors have different quarter ends (IBM’s is December, HP’s October and Cisco’s January, so we’ll also have to weigh each of their results against the calendar year for our comparisons.

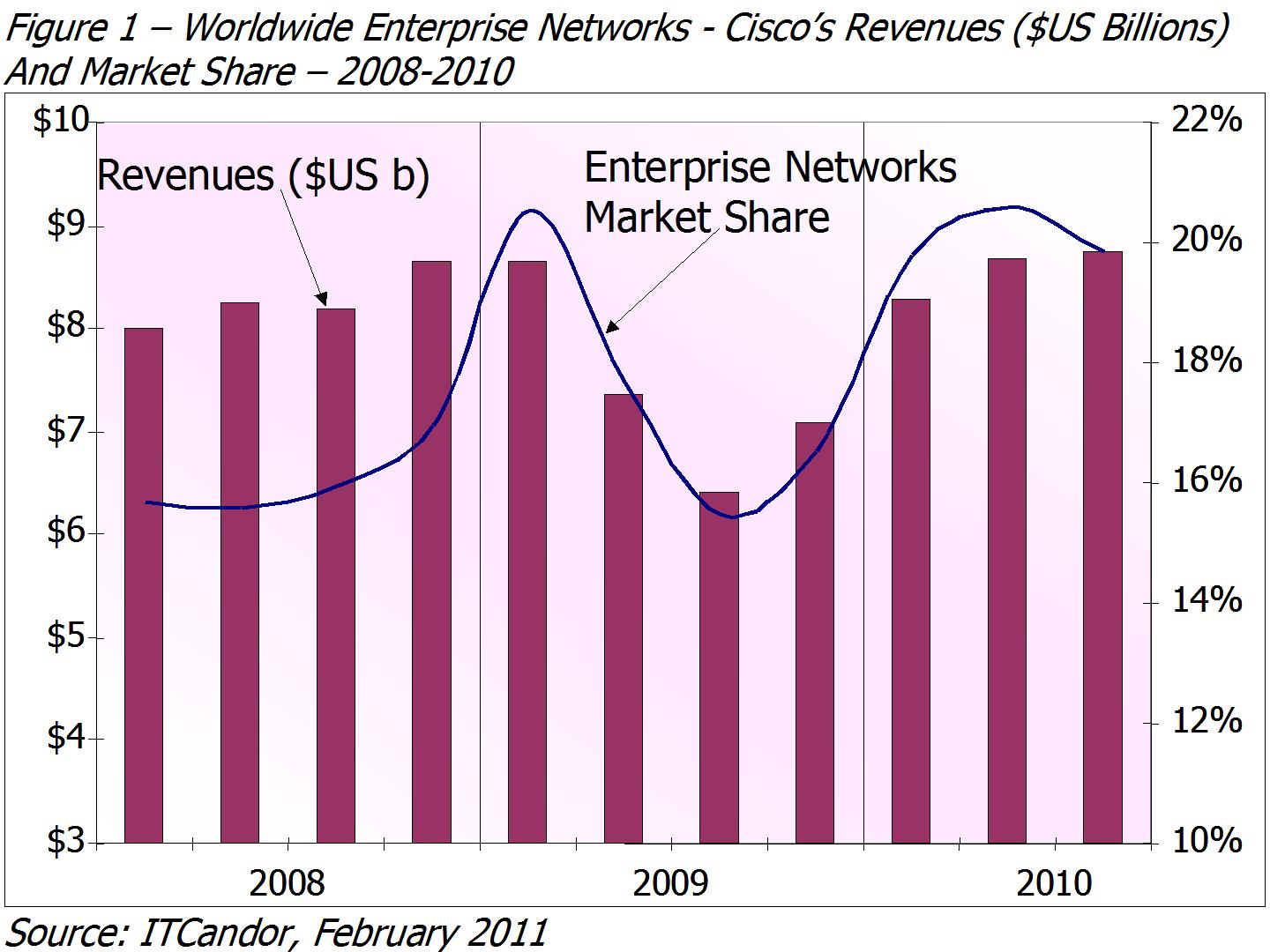

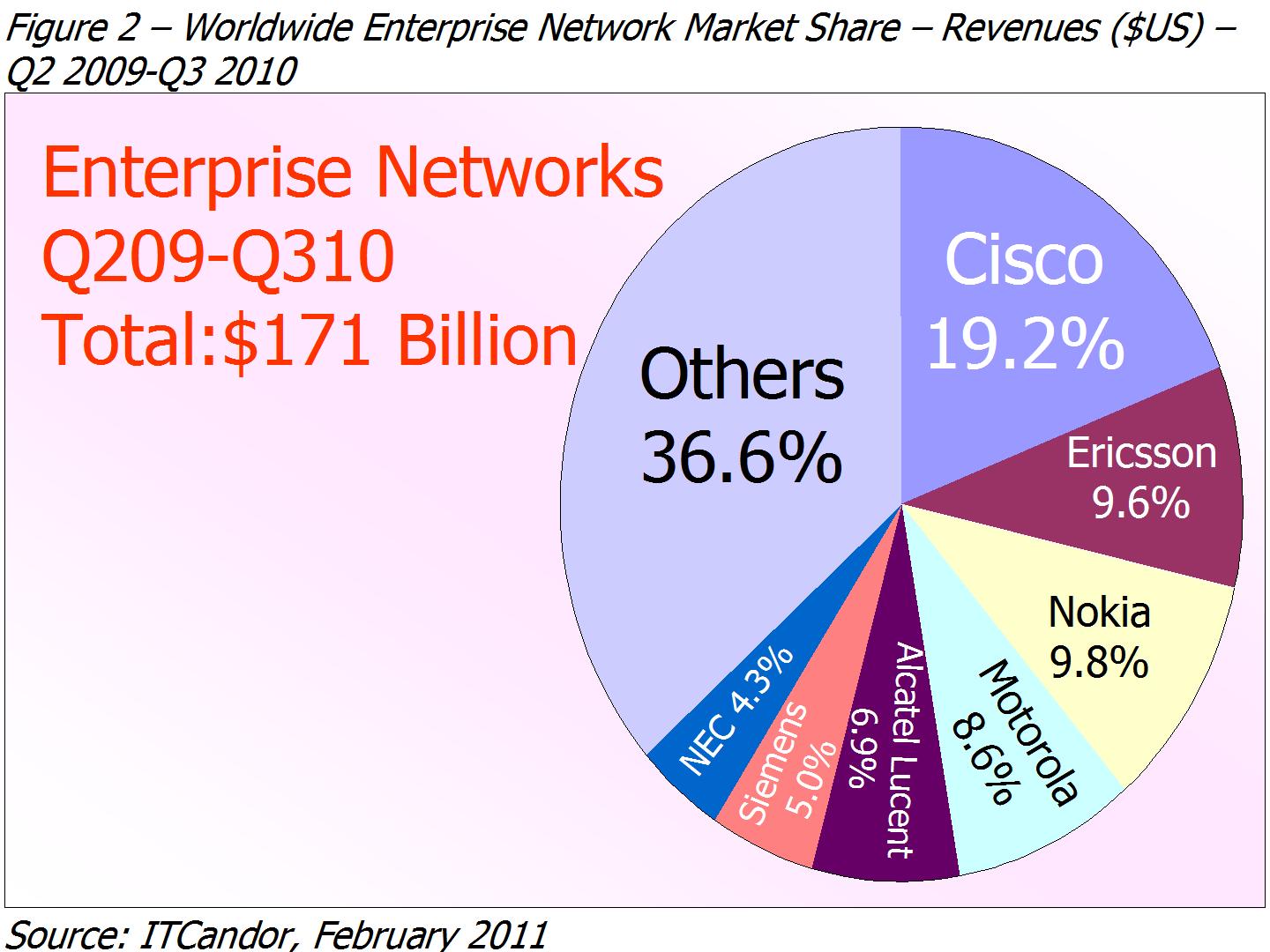

Despite Cisco’s diversification it still generates a high proportion of its revenues from switches (33% in the last reported quarter) and routers (16%) – see Figure 1 and 2 for its revenues and market share in the over all ITC Networks market worldwide – Cisco has a much bigger share of the Enterprise Network market of course. Products in total accounted for 81% of revenues, while service was 19%. We believe 80% of its sales are made through third parties, with a third of those through Telecoms companies, which we classify as ‘indirect single tier’ and others (including Cisco) often call ‘service providers’.

On a geographic basis the Americas are Cisco’s largest sales area, accounting for 55% of its last reported quarterly results, EMEA was 30% and Asia Pacific, 15%. Beyond these standard accounting regions the company maintains one of the best approaches we have seen to emerging markets – addressing each country individually as part of its overall strategy. Things have moved on from a few years ago, when its entry often involved helping the government establish data networks for the first time as part of a quasi-CSR approach. Of the many countries in which it’s building business we believe Brazil is one of the fastest growing.

{kind=link}

{kind=link}

Cisco Addresses New Generational Internally – What About Younger IT Purchasers?

Like many CEOs Chambers does his best to accommodate generational issues in his management style – his approach might best be described as ‘study what the kids are doing and adopt it’. Chris Dedicoat (head of Cisco Europe) presented a recent research study in which Cisco asked 19-24 year olds about the most important things ‘they couldn’t do without’. In the results

- Mobile phones came top (97%), followed by

- The Internet (84%),

- A car (64%)and

- Their current partner (43%).

It paints a clear picture of the importance of technology to ‘Generation Y’.

John shared an interesting anecdote with us about a time when travelling by plane and working with his management team. The network broke, making it impossible to use Internet sources for analysis, so he suggested they use the paper copy of the Wall Street Journal he had with him instead. That this was a new process to them was demonstrated by the fact they didn’t know how to use the index (he also noted that they pulled it apart into 4 pieces).

Although observing that he managed 10k people at the age of 40, John made the point that he (and CEOs in other IT companies) have been able to grow along with their organisations. To accommodate new generation staff John changed its structure in 2005 – moving away from a ‘command and control’ structure, which he admits comes more naturally to him.

We are more interested in the way that new generational issues change IT purchasing behaviour. Being absent from the consumer market, Cisco is behind Apple, RIM and Google: these competitors almost certainly understand the degree to which prosumers will change market demand in coming years.

Should Cisco’s UCS Accommodate The Shift Towards Workloads And Appliances?

We had the opportunity to talk to Cisco about UCS – a server offering available in rack and blade form factors, complete with Cisco management software. We have the impression that the company is building its business on the premise that this is a general-purpose product, just at the time when HP and IBM (the largest server vendors) are experimenting with appliances and workload-optimized systems. It was at least clear from our discussion with John and others that workloads are not yet particularly strong component of its server business. While most of Cisco’s overall strategy is strongly associated with ‘collaboration’ in general, in the server market IBM narrows the definition to apply to email and similar activities, while HP and Microsoft would normally refer to the same workload as ‘messaging’.

Back in November Cisco, EMC and its subsidiary VMWare announced they were forming a new company called Acadia to sell Cloud systems based on Cisco UCS blade servers, EMC storage gear, VMware virtualization software and EMC Ionix management software. They also use BMC management software. Having appointed ex-Compaq head Michael Capellas as CEO, the company has already changed its name to VCE. We would not classify this as an appliance or workload approach.

Interestingly John talked about the difficulty of forming alliances (far harder than building business through acquisition of doing it yourself). We don’t know whether or not this was an oblique reference to VCE/Acadia: he did note that in the past the company was frustrated when a different alliance failed to drive sales sufficiently.

Does Cisco Need An Overall Mission Target As Well As Its Five Architectures?

We are impressed with the way in which Mark Templeton at Citrix has driven his organisation through acquisition to become an ‘Application Access’ company and the way that EMC redefined itself as a ‘Content Management’ supplier. The same is not true of Cisco. It has five ‘architectures’, which are:

- Boarderless networks

- Collaboration

- Data Centre and Virtualisation

- Service Providers

- Security

These are certainly reasonable product and service areas for the company, demonstrating how far it has come from the more narrowly defined enterprise network supplier it was 10 years ago. John talks about the evolution of the concepts Cisco developed over the years. In particular:

- 1997 – the unification of data, voice and video

- 2000 – the ‘network of networks’

- 2006 – the network as the platform

- 2008 – collaboration/Web 2.0

- 2010 – ‘the networked economy’

However this is different from having an overall framework into which the company builds its offerings and services. We’re not sure whether the lack of a simple binding vision will be a hindrance to Cisco going forward – after all neither IBM nor HP have one either.

Will Cisco’s Strong Ties Help Win Cloud Computing Deals With Telecoms Service Providers In Europe?

We talked to Cisco about its developing Cloud Computing offerings. It was also very useful to hear from its customer Cable & Wireless in the same session (perhaps I can claim to be one of its first ever Cloud Computing customers having helped Inteco set up a mail box service in the early 1980s).

Cable & Wireless has 2 data centres in the UK (including one in Basingstoke) from which it runs IaaS services mainly to its existing customers. Its services are multi-tenant and are currently all base on its MPLS services. This is less expansive than other Cloud Computing services, such as those run by Virtustream or Fujitsu, but will certainly challenge data jurisdiction issues less strongly than Amazon or Google’s current solutions.

Beyond – and including – the VCE/Acadia play it is significant that Cisco has very strong connections with Telecoms suppliers in Europe, who we see are taking the early lead in becoming Cloud Computing service suppliers. Its ties are stronger than Sun, HP and IBM, despite their previously strong Unix server revenues from the Telecoms sector. We believe there will be strong competition between all four suppliers and intend to profile their Cloud Computing strategies in more detail later. In the end it may not matter which Cloud Computing Strategy Cisco follows, since it will be a significant part of almost all implementations: the other systems suppliers either have to partner with them (IBM and EMC) or produce their own networking components (HP, Oracle).

Some Conclusions – Integration Challenges, Cloud And Network Wars

Cisco is a dominant supplier in the Enterprise Networks market. In fact, despite its own diversification and increasing competition from HP as a network supplier, it has managed to increase its market share over the years. However its success may become its Achilles’ heel. In the new market the power of the ‘horizontal component’ vendors like Intel, Microsoft and HP is likely to diminish in favour of the ‘vertically integrated’ ones such as Apple, IBM and RIM. We can already see the downgrading of Open Source developments since the recession and this may spread to suppliers who fail to simplify and offer integrated solutions, which necessitates successful partnering: time will tell whether HP’s with Microsoft or Cisco’s with EMC and VMWare can compete in the data centre.

Cisco has tremendous advantages in already selling to most Telecom companies – at least in Europe where they are investing rapidly to become Cloud Computing service suppliers. It should be able to pioneer the development of new aggregator channels as a result. John Chambers has also readied his company for Generation Y management – it will be interesting to see the extent to which it can follow Generation Y changes in customer purchasing behaviour.

Are you a Cisco customer? How do you see the company as a supplier? Please let us know by commenting on this article.

ITCandor Acronym Buster

CSR- Corporate and Social Responsibility

EMEA – Europe Middle East and Africa

Generation Y – the children of the children (Generation X) of the Baby Boomers

prosumers – consumers adding content to the Internet

RIM – Research In Motion

UCS – Unified Computing System

VCE – Virtual Computing Environment

Web 2.0 – newer Internet companies

Martin, your enterprise network category is a mix of enterprise and service provider networks. Nokia (i guess you mean Nokia Siemens here), Ericsson, Motorola and NEC are insignificant in enterprise networks. More relevant are HP, Juniper, Brocade, and Extreme. Cisco enterprise network market share is closer to 70% I would think.

Pim

Pim

Thanks for your comments as always.

You’re right of course. I’m waiting for all the Q4 numbers to ccome in before publishing an update. Yes on Nokia Siemens Networks by the way and I have all of the companies in my model of course – probably need to retitle the market share as just ‘Networks’.

Best Wishes

Martin

Cisco’s quarterly revenues actually only grew 6% to $10.4 billion – so I was overly optimisitc in my forecast above.

Maritn